Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Heading into the fall last year, the average 30-year fixed mortgage rate slipped to a low of 6.07% by September 17, 2024 as the market reacted to weaker than expected labor market data. At that point, there was a noticeable upswing in refinances as some 2022–2024 borrowers took the opportunity to get payment relief.

However, it was short-lived and quickly fizzled out once labor market data tightened a bit and mortgage rates popped back up.

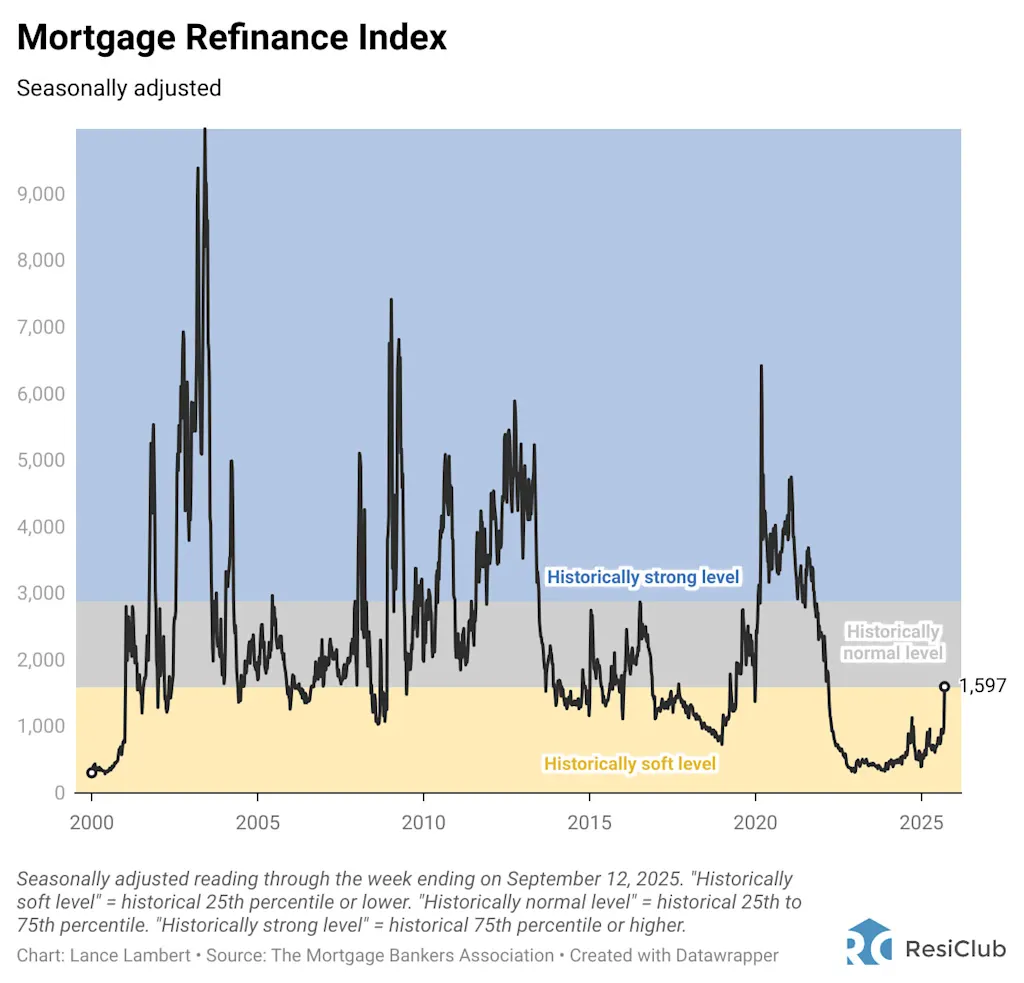

Fast-forward to September 2025, and we’re once again seeing a mini “refi boomlet.”

Similar to early last fall, the average 30-year fixed mortgage rate has fallen a bit heading into September—with the average 30-year fixed mortgage rate hitting a calendar year low of 6.26% last week, according to Freddie Mac’s weekly reading.

With the average 30-year fixed mortgage rate sitting well below 2025’s calendar-year high of 7.04%, some recent borrowers are taking the opportunity to refinance and gain some payment relief.

The Mortgage Refinance Index reading for the second week of September, by year:

- September 14, 2018: 917

- September 13, 2019: 2,274

- September 11, 2020: 3,289

- September 10, 2021: 3,186

- September 9, 2022: 533

- September 8, 2023: 367

- September 13, 2024: 941

- September 12, 2025: 1,597

If you look closely at the chart above, you’ll notice that last year’s peak weekly reading for the Mortgage Refinance Index (1,133 on the week ending September 21, 2024) is well below the reading we just saw for the week ending September 12, 2025—even though mortgage rates last September dipped slightly lower than they did this September.

The reason this September’s refi boomlet is likely bigger than last year’s is that many borrowers who held out for a larger rate drop last fall were burned when mortgage rates jumped back up late in 2024. So when the opportunity for payment relief came around this year, many jumped on it.

You may have noticed that ResiClub calls this a “refi boomlet” rather than a “refi boom.”

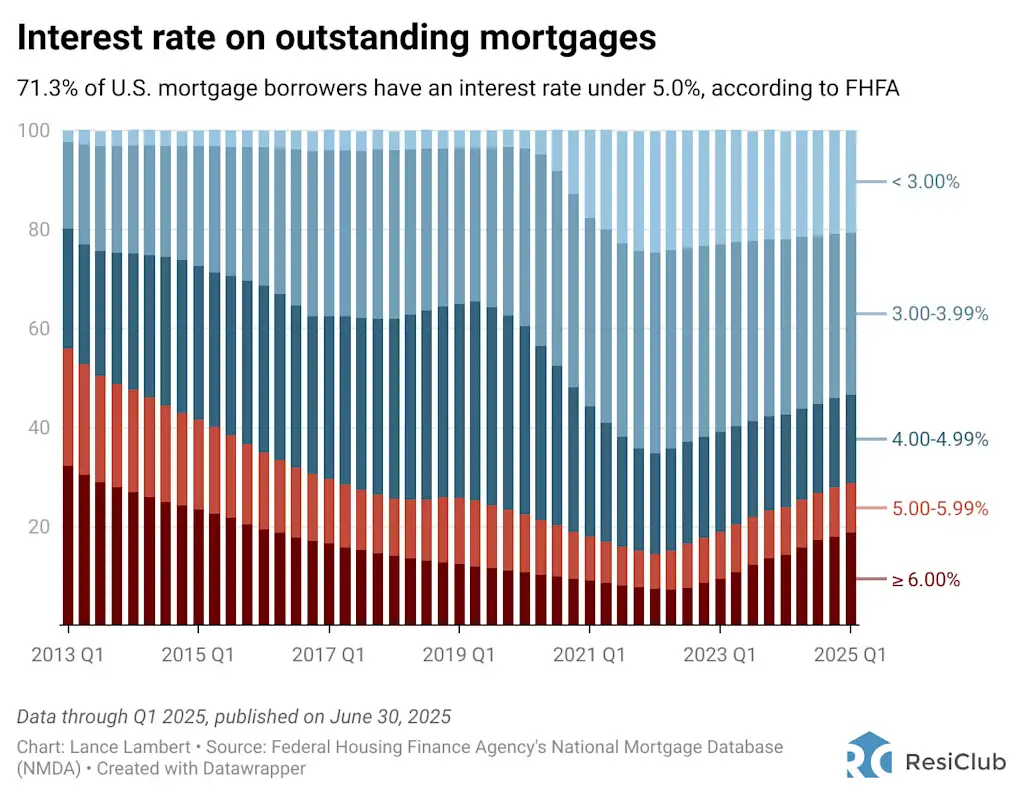

We use the term boomlet because there’s a ceiling on how big this refinance pop can get—and how long it can last—without a much more substantial drop in mortgage rates. After all, according to the latest FHFA data, 71.3% of U.S. mortgage borrowers still hold an interest rate below 5.0%.

How far would mortgage rates need to fall to spur a real refi boom? Read this ResiClub article.

Related Posts

Popmart has paused all Labubu sales in the UK for safety reasons amid the blind box craze

Pop Mart has temporarily paused Labubu sales in the UK.…

Forget the food delivery war — Alibaba makes clear the real play in China is AI

People visit an Alibaba booth at an exhibition in China.…

I founded Bala after a burnout recovery trip — but burned out again. Here’s how I cope now.

Courtesy of Natalie Holloway; Rebecca Zisser/BI Natalie Holloway found her…